To understand customers’ buying habits, first understand what makes them tick

December 9, 2021

SCOR’s behavioral science teams investigate the biases driving insurance purchases, to transform the insurance journey

Take a look behind the scenes of the insurance industry and you’ll find behavioral science teams hard at work uncovering new ways to meet policyholders’ needs.

“Behavioral science is the intersection of economics and psychology,” explains Aisling Bradfield, Head of Behavioral Science at SCOR. “Experimentation provides insights into real human behavior and how this differs from what we might consider ‘rational behavior’ under standard economic theory.”

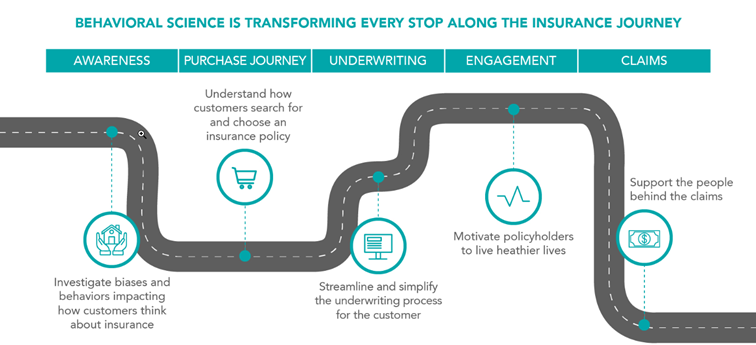

Behavioral science may not be the most visible field in the insurance sector, but it has the potential to transform every stop along the insurance journey, by simplifying and streamlining the application process, ensuring applicants find the right policy for their needs, and improving engagement.

1. Understanding biases and behaviors

Why are people willing to cover their bike against theft or buy an extended warranty for their new laptop – which costs a few hundred dollars to replace if stolen or damaged – yet they won’t purchase health or home insurance, which could completely wipe out their life savings in the case of an emergency?

In France, a longstanding partnership between the SCOR Foundation for Science and the Toulouse School of Economics (TSE) is working to understand this and other inconsistencies between customers’ needs and their purchasing decisions.

One factor is that individuals’ perception of risk is skewed. Low-impact risks (like having your bike stolen) are perceived as more probable and therefore more beneficial to insure than low-risk, high-impact events (like your house flooding).

As Aisling explains, our preference for short-term gratification over long-term results is also to blame: “Risks in the present are feared more than those in the future. It is more difficult to think about our future selves.”

By understanding the misconceptions and aversions behind these inconsistencies in customers’ behavior, insurers can ensure their customers understand their needs more fully and are covering the low-likelihood, high-consequence risks that actually matter to them.

Learn more about the work being done by SCOR and TSE

2. Understanding customer preferences

Imagine you’re purchasing life insurance. Which product do you choose? Do you want a lump sum or income benefit? Are you interested in a health and wellness program? What about survival benefits? How much extra would you be willing to pay for the features you find most attractive? Through years of product innovation, there are many options out there, but do insurers really know what customers prefer?

SCOR and Nanterre University in Paris have teamed up to design a discrete choice experiment (DCE) that aims to understand customer preferences in order to help insurance companies design products more efficiently.

The experiment offers participants a choice between two policies with different features. Once participants have responded to a series of these choice pairs, the team is able to analyze the patterns in their responses to understand which criteria are most important to customers. The results of this study are expected to be released in 2022.

3. Redesigning underwriting

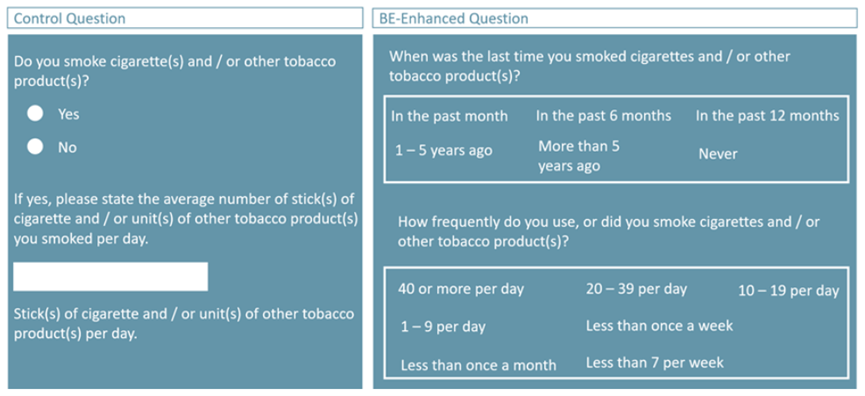

SCOR believes that, rather than viewing improved underwriting journeys as a trade-off between more accurate disclosure and quicker completion times, behavioral science can offer solutions that deliver both. This starts by understanding what can lead applicants to provide inaccurate information. Oftentimes, this is unintentional and can be influenced by several factors:

| Framing | People will answer differently depending on how the question is presented |

|---|---|

| Honesty Beliefs | People will only be dishonest to the point where they can still feel good about themselves |

| Cognitive Resources | People do not want to do more work than is necessary; they would often prefer to guess the answer to a question than search for further information |

| Negative Behaviors | People may not want to admit socially unacceptable behaviors or truths |

Knowing this, we can design questionnaires to minimize the need for additional effort on the customer’s side, while also presenting questions in such a way that the applicant doesn’t feel they will be judged or penalized for answering honestly.

The approach was supported by a recent case study from SCOR Global Life and Nanyang Business School in Singapore, which found that three times as many people declared themselves as smokers when the questions asked were formulated differently:

4. Helping policyholders live healthier lives

Traditionally, insurance has been a one-and-done purchase, but as insurers are increasingly stepping up as health and wellness leaders, they are looking for ways to help policyholders on an ongoing basis by encouraging them to live healthier, longer lives.

Traditionally, insurance has been a one-and-done purchase, but as insurers are increasingly stepping up as health and wellness leaders, they are looking for ways to help policyholders on an ongoing basis by encouraging them to live healthier, longer lives.

“Behavioral science can also play a role here and has been part of our discussions around the Biological Age Model,” says Aisling.

The Biological Age Model, or BAM, is an algorithm that translates the number of daily steps and overall physical activity into a reduction in age, turning long-term goals into immediate results and encouraging user engagement. The BAM algorithm is brought to life by platforms such as the Good Life app, developed by SCOR’s subsidiary Remark.

BAM creates engagement through the concept of loss aversion, the idea that people are more motivated by avoiding losses than achieving gains. Even without offering a financial incentive, people are motivated to maintain their Biological Age so that they don’t “lose” the extra years of life they have earned. And the fact that the reward (a younger Biological Age) is immediate appeals to our desire for instant gratification.

5. Better support policyholders during the claims process

The same behavioral science concepts behind this approach to underwriting can be applied to ensure a streamlined claims process. People making claims have generally either just suffered a medical emergency or a death in the family, so we understand that they are likely stressed and emotionally drained. They don’t want to sort through a claims process riddled with confusing questions and they’re certainly not going to want to take the time to do extra research to make sure they are answering accurately. Still, it’s important that insurers receive the most accurate information possible in order to process claims efficiently.

To address these concerns, SCOR’s Claims Rules Engine (CRE) offers a simple and intuitive digital claims experience for insurers and their customers. This ensures that claims are less taxing for the insured and that the insurer receives more accurate information.

Discover how our Claims Rules Engine

simplifies the claims process – for policyholders and insurers

In markets around the world, SCOR’s teams are applying behavioral science concepts to improve the insurance process, and at every stop along the insurance journey these changes are benefiting both insurers and policyholders. Keep an eye out for upcoming new projects and insights in 2022.